How To Make Your Money Work For You

How To Make Your Money Work For You

6 essential investing principles everyone should follow

extras besides living expenses and don’t have money left after paying rent and grocery shopping.

Financial Literacy is inherited. If your parents aren’t smart about money, chances are high that you don’t know essential investing principles.

I started with no know-how in January 2016. But I committed: I took masterclasses, connected with financial experts, read 12 finance books, and attended conferences.

Four years later, I can say money management and investing is a skill you can learn. And it doesn’t have to take you four years to mastery.

Follow these essential principles, and you’ll find yourself on your path to making your money work for you.

1.) The best investment you can make is an investment in yourself.

You are the one in charge of every decision in your life. You are responsible for your worst and your best investments.

When was the last time you bought expensive consumer goods you barely used? What helped you making your best investment decisions like that ETF savings plan in your depot? Probably investments in your education.

Since you make all financial decisions in your life, it makes sense to invest in yourself: the better your knowledge, the wiser your choices.

“An investment in knowledge always pays the best interest.”

— Benjamin Franklin

How to apply it:

Set 50$ aside every month to invest in books, masterclasses, or seminars.

I scanned through “popular finance books” sections and ordered the most appealing. On my shelf, you’d find The Intelligent Investor, Think and Grow Rich, or The Millionaire Next Door. I listened to audiobooks like “Rich Dad Poor Dad,” and after covering the basics, I dived deeper with expert guides on real estate investment and ETF strategies.

2.) Your salary won’t make you rich but your spending habits will.

Your salary won’t determine whether you become rich or poor. It’s your spending habits that influence your wealth.

Wealth isn’t about how much you make. It’s about how much you save.

Regardless of whether you have $1200 or $9500 on your salary slip, by spending 95% of it on consumer goods, there isn’t enough left to grow your money.

“We buy things we don’t need with money we don’t have to impress people we don’t like.”

— Dave Ramsey

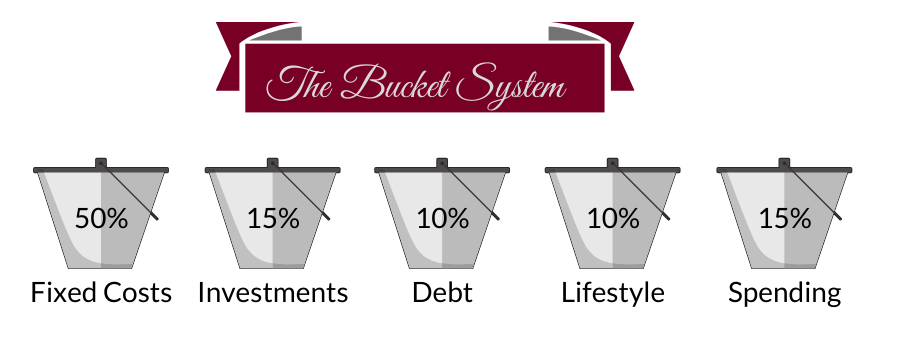

Instead of wasting most of your income on consumer goods, split your income to specific buckets.

Splitting Your Income According To a Bucket System (Source: Author).

Fixed Costs are the costs that occur monthly (rent, electricity, water, internet, phone). For investments, there is a possibility of an increase in value in the long-term future (stocks, bonds, real estate, commodities). Paying your debt is self-explanatory.

Lifestyle includes all expenditures that go along with pure leisure and don’t serve any educational or investing purpose. The spending bucket covers groceries, local transportation tickets, and car costs.

The percentage of your income you spend on each bucket is up to you. But you should make a conscious choice on how much to spend for each bucket.

Remember, it isn’t your salary that makes you rich. It’s your spending habits.

How to apply it:

Many people track their spending habits with apps like Mint, Monefy, Wallet, or Goodbudget.

I also used an app for a few weeks, but then I stopped. It felt inconvenient to log in every expense. Instead, I built separate accounts around the bucket system.

Here’s how I split my paycheck into four accounts: I leave 50% for fixed costs on my paycheck account. By permanent transfer, 15% move from my paycheck account to a separate spending account. With another permanent transfer, a 15% move to my N26 account for lifestyle expenditures. It’s connected to Apple Pay, and I use this account for eating out; coffee-to-go or shopping. This system helps me keep an overview of my expenditures. The remaining 20% move to my investment system, more on that later.

3.) You can’t avoid risk if you want to invest successfully.

Are you looking for a risk-free investment that rewards you with growing dividends? It’s like saying you want ice-cold hot water. You should be highly skeptical if somebody tries to convince you of the opposite.

Risk and return are interrelated. The money market rewards investors with an interest in the risks they take.

Therefore, successful investing isn’t about avoiding risks and profits.

Instead, intelligent investing is about diversifying your risks. Here comes the classical “don’t put all eggs in one basket” advice. But it’s true.

Split your investments into different asset classes with varying risk profiles. A part of your investment portfolio should be risk-free and liquid.

A rule of thumb: 100-your age = % of your riskier investments

Asset Classes: Potential Return and Expected Risk (Source: Europhoenix).

How to apply it:

Be clear about what you might gain and what you might lose. Be aware that you don’t like to lose things. Daniel Kahneman, famous for behavioral economics, has proven human loss aversion, meaning you prefer avoiding losses over acquiring equivalent gains.

Before I invest, I always ask myself, “What’s the worst case that can happen with this investment? How will this affect my life? Am I able to bear the loss?”

Only if the worst outcome feels bearable, I invest. Thereby, I prevent myself from the beginner’s mistake of pulling money out of a market when it reached the bottom.

4.) Don’t save what is left after spending — spend what is left after saving.

This is probably the most important advice I ever received. Remember, you won’t become wealthy if you spend 95% of your salary on consumer goods?

Smart investors save before spending.

On the same day that your salary arrives in your account, you should make all planned investments.

Only after you invested the amount you planned to invest, consider buying consumer goods.

Only spend what is left after saving.

How to apply it:

Set up a default option that prevents you from spending your investment money. A system that automizes your investments.

I invest 20% of my income. From my paycheck, 12% move to ETFs, 5% to cryptocurrencies, and 3% in lower-risk assets like bonds. On top of the 20%, I occasionally join the gambling game by cherrypicking stocks. For stock-picking, I use money from my lifestyle bucket.

5.) One year from now, you’ll wish you started today.

The best time to start investing was yesterday. The second best is today.

If you are new to personal finance, start with investments in yourself.

Don’t start by talking to your bank’s financial advisor. Bank advisors are your bank’s salespersons. They do earn money with commissions. 0.2% costs may seem small, but if you consider compounding, bank advisor is very costly.

How to apply it:

To master investing, make sure there is space in your life for it, and be sure to enjoy the journey. Dedicate time and make learning a routine.

To learn about investing, you can start with any of the following:

Start and finish an online course that resonates with you by searching terms like “financial education online course” or “investing for beginners.”

Ask your friends about whether they can give advice or recommend books on investing. Still, cross-check before following any direct investment advice.

Listen to finance podcasts or check out blogs on “financial freedom.”

6.) Investing failure comes down to two things:

#1 Doing things without thinking about them.

If you follow the advice, “the best investment you can make is an investment in yourself,” you can avoid the first trap.

As an educated, informed decision-maker, you think first before you invest.

#2 Thinking about things without doing them.

I invested more than 350 hours in my financial education. But only after halfway in, I felt brave enough to act on my knowledge.

If you overthink and wait for too long, you will regret not having started investing earlier.

“The way that people build true wealth for themselves is they see money differently than everyone else. They don’t see it as something they “have.” They see it as something they deploy, and use to build and grow from there.”

Are you ready to make your money work for you? Here’s an excellent piece of advice by Nicolas Cole

Excellent advice concerning money investment , thank you a lot .